For real estate agents, affordability conversations have become harder. Buyers are watching mortgage rates, sellers are watching list prices, and everyone is trying to make sense of monthly payments that still feel stretched. But one cost often enters the conversation too late: homeowners association dues, condo fees, or required community association fees.

That late surprise can create real friction. A buyer gets excited about a condo, townhome, or planned-community single-family home. The list price looks manageable. The mortgage estimate looks close enough. Then the HOA line appears, and the monthly payment no longer fits the budget. The buyer may pull back, widen the search, ask for a price concession, or start comparing properties in a different way.

For agents, the opportunity is straightforward: bring HOA into the affordability conversation earlier. Not as a scare tactic, and not as a reason to dismiss homes with fees, but as part of a more complete monthly-cost analysis.

HOA fees are not automatically negative. In many communities, they pay for real services: exterior maintenance, landscaping, pools, elevators, building insurance, security, trash service, private roads, reserves, shared amenities, or common-area upkeep. A $300 monthly fee may be reasonable if it covers costs the owner would otherwise pay directly. A $75 fee may be less attractive if it covers little or signals underfunded reserves.

The issue is that buyers often compare homes by list price first, mortgage payment second, and HOA third. That order can distort affordability. The Consumer Financial Protection Bureau says condo, co-op, and homeowners association dues are usually paid directly to the association and are usually not included in the payment made to the mortgage servicer. CFPB also warns that dues can range from a few hundred dollars per month to more than $1,000, and buyers should factor them into affordability.

That makes HOA a practical advisory topic for agents. It affects search filters, buyer qualification, offer strategy, property comparisons, and expectation-setting. It can also affect how sellers and listing agents position a property when the fee looks high but includes meaningful services.

To understand how different this issue looks by market, we analyzed eight major metros:

- Miami

- San Diego

- Las Vegas

- Chicago

- Phoenix

- Dallas

- Austin

- Orlando

The data shows that agents should not treat HOA as one simple category. In some markets, the problem is high fee size. In others, it is high prevalence. In others, a moderate fee consumes a surprisingly large share of the modeled monthly payment.

For agents, the headline is this: HOA is not just a fee. It is a monthly-payment variable that can change how buyers compare homes.

Try AI Web Scraper for Real Estate Market Research

Why Agents Should Lead With Total Monthly Cost

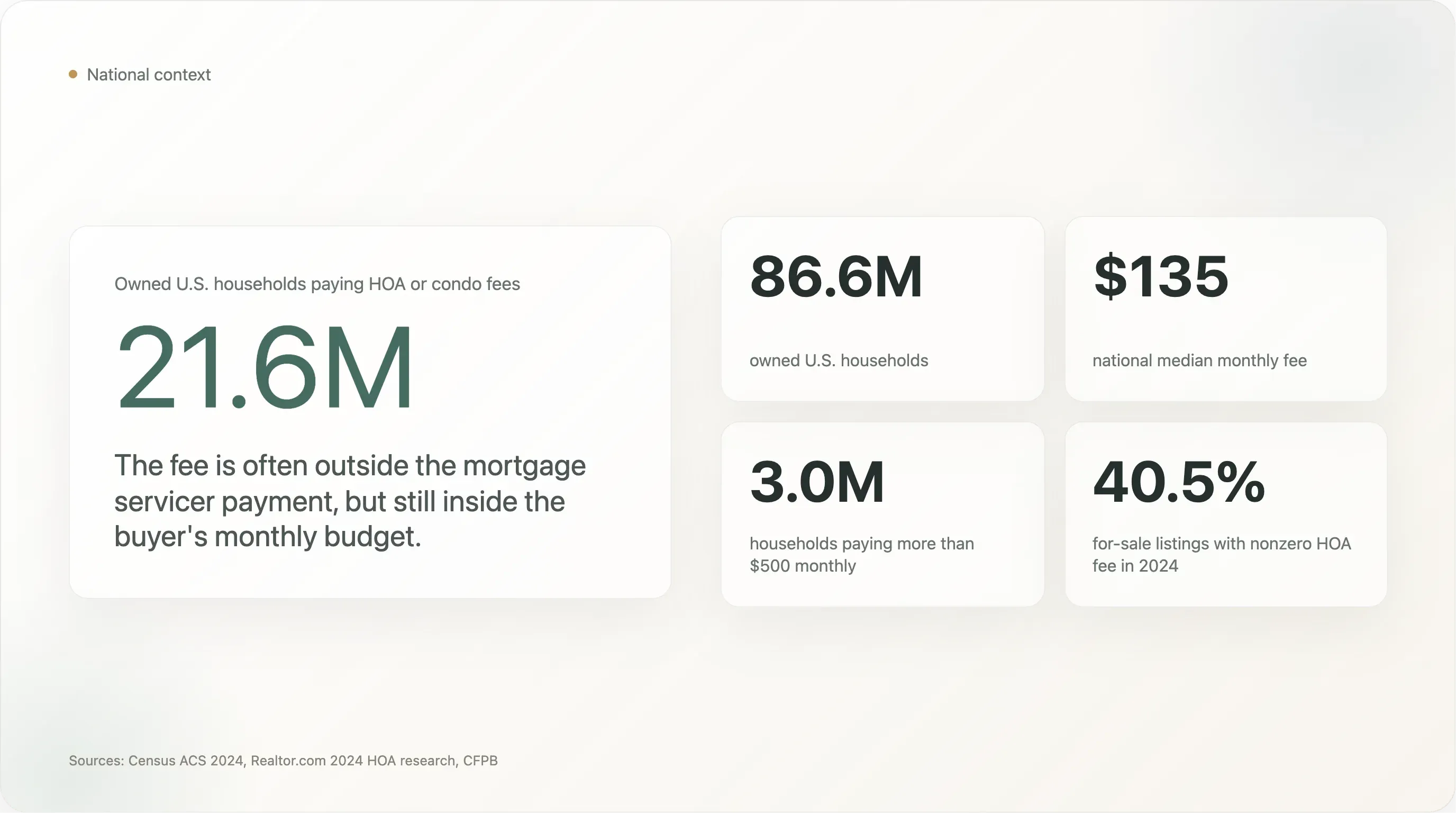

HOA and condo fees are no longer niche costs. The Foundation for Community Association Research estimates that more than one third of U.S. housing is in a community association, with 373,000 community associations and 78.1 million residents in the U.S.

The Census Bureau's 2024 American Community Survey gives a clearer view of the issue. Beginning in 2024, the Census Bureau revised its condominium questions to include homeowners association status and fees. Census cautions that users cannot separate HOA fees from condo fees in the reported monthly amount. For agents, that limitation is important, but the buyer-facing point remains the same: whether the fee is called HOA dues, condo fees, or association fees, it is still a required monthly housing cost.

Nationally, Census reported that about 21.6 million of 86.6 million owned U.S. households paid either a condo or HOA fee in 2024. The national median monthly fee was $135, and about 3 million households paid more than $500 per month.

Realtor.com research shows the same trend from the listing side. In 2024, Realtor.com reported that 40.5% of for-sale listings had a nonzero HOA fee, up from 39.2% in 2023, with the median monthly fee rising from $110 to $125. Realtor.com also found that new construction listings were much more likely than existing homes to have monthly HOA obligations, and condo, rowhome, and townhome listings were especially likely to carry dues.

That matters for agent-client conversations because buyers rarely experience affordability as an academic metric. They experience it as a monthly payment threshold. If a buyer is trying to stay under $3,000 per month, a $250 HOA fee is not background noise. It may be the difference between a comfortable search and a difficult one.

Agents who can explain that clearly are not just sharing data. They are helping buyers avoid late-stage disappointment.

Methodology

This is a low-cost public-data study designed for practical market education. We did not scrape MLS login data, bypass paywalls, solve CAPTCHAs, or bulk extract individual listing pages. We used public and downloadable sources:

- U.S. Census Bureau 2024 ACS 1-year tables B25142 and B25143 for metro-level HOA and/or condo fee prevalence, median monthly fee, and fee distribution.

- Realtor.com Economic Research monthly metro inventory CSV for April 2026 listing price, active inventory, median days on market, and price-reduced share.

- Freddie Mac PMMS, which showed the 30-year fixed-rate mortgage at 6.30% as of April 30, 2026.

- CFPB consumer guidance on HOA and condo dues.

- Foundation for Community Association Research national community association statistics.

Important distinction: ACS data measures owner-occupied households that pay required HOA and/or condo fees. It is not active-listing data. Realtor.com data is used for current market context, such as median listing price and price-reduction share, not to claim that every listing in the metro has the ACS median HOA fee.

For the affordability model, we used:

- 20% down payment

- 30-year fixed mortgage

- 6.30% annual interest rate

- Principal and interest only

- Excludes taxes, insurance, mortgage insurance, utilities, maintenance, and closing costs

This model is intentionally simple. It isolates the monthly effect of HOA or condo fees. It is not a full buyer qualification model and should not replace lender guidance.

At 6.30% over 30 years, every $100,000 of loan principal creates about $619 in monthly principal and interest. That conversion lets agents translate HOA fees into a more intuitive buyer conversation: "This monthly fee has about the same payment impact as adding roughly X dollars to the purchase price."

The 8-Metro Snapshot

Across the eight metros in this study, ACS counted about 9.44 million owner-occupied households. About 4.17 million of them paid a required HOA and/or condo fee in 2024. That means 44.2% of owner-occupied households across this sample paid some form of required association or condo fee.

The eight metros also include about 611,000 fee-paying owner households with monthly fees of $500 or more. For agents, this high-fee group is important because $500 per month can materially change buyer behavior. It can reduce budget, trigger lender questions, complicate condo affordability, or make a lower-priced property feel less affordable than expected.

Here is the core table:

| Rank | Metro | ACS median HOA/condo fee | Owners with fee | $500+ among fee payers | Realtor median listing price Apr 2026 | P&I @20% down, 6.30% | HOA share of P&I+HOA | HOA equivalent purchase price | Price-reduced share | Median DOM |

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Miami | $410 | 54.1% | 39.5% | $499,250 | $2,472 | 14.2% | $82,798 | 15.7% | 77 |

| 2 | San Diego | $277 | 38.3% | 16.8% | $933,325 | $4,622 | 5.7% | $55,939 | 14.9% | 38 |

| 3 | Chicago | $252 | 30.5% | 16.2% | $375,000 | $1,857 | 11.9% | $50,891 | 10.1% | 34 |

| 4 | Orlando | $125 | 56.4% | 6.6% | $419,000 | $2,075 | 5.7% | $25,243 | 20.8% | 68 |

| 5 | Phoenix | $106 | 54.0% | 3.6% | $499,000 | $2,471 | 4.1% | $21,406 | 29.1% | 57 |

| 6 | Las Vegas | $99 | 60.9% | 3.1% | $474,950 | $2,352 | 4.0% | $19,993 | 21.6% | 51 |

| 7 | Dallas | $75 | 37.5% | 9.7% | $430,000 | $2,129 | 3.4% | $15,146 | 22.1% | 46 |

| 8 | Austin | $62 | 52.9% | 4.6% | $475,000 | $2,352 | 2.6% | $12,521 | 23.6% | 51 |

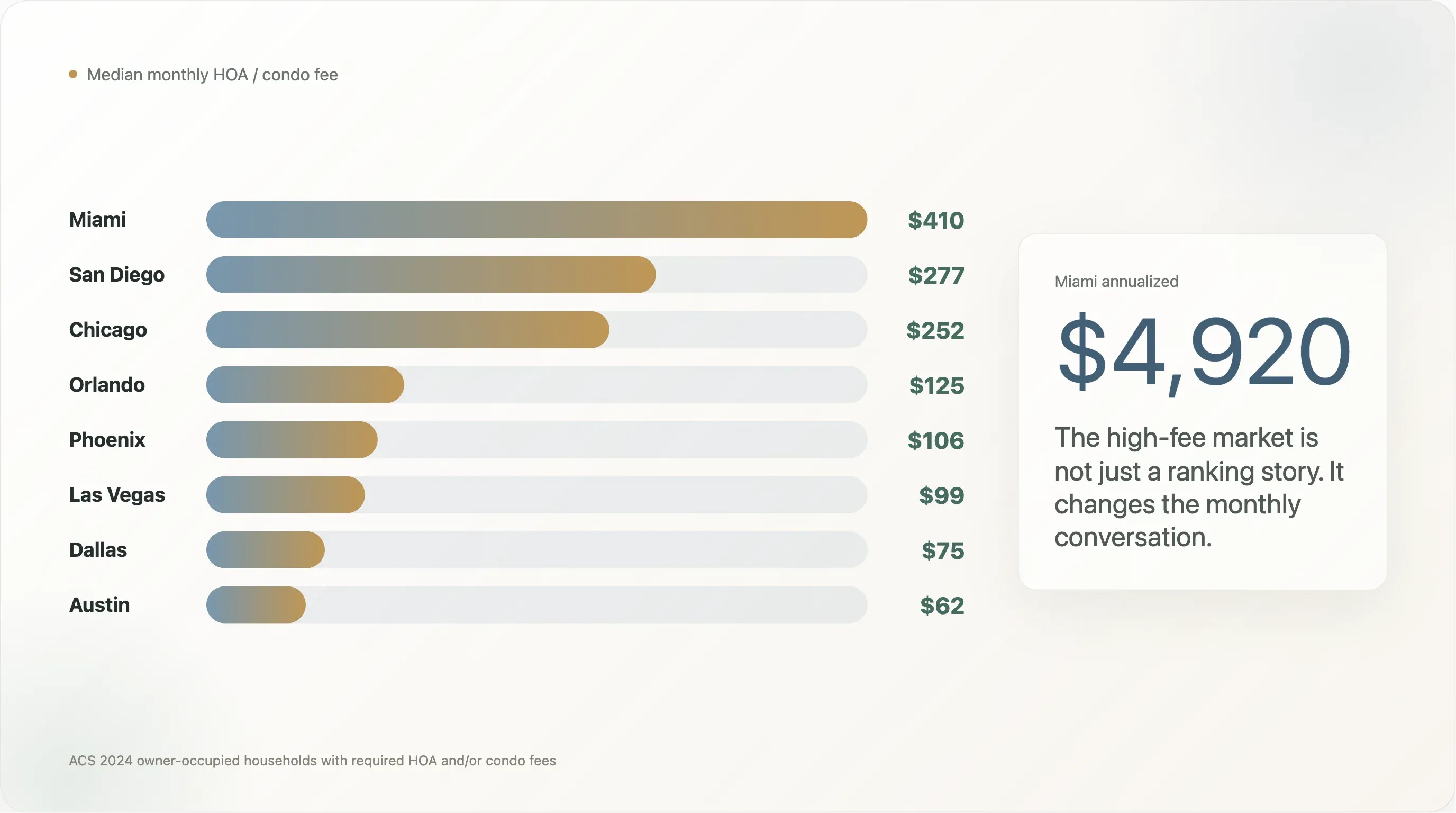

Miami stands out on fee size. Its ACS median monthly HOA and/or condo fee is $410, far above every other metro in the sample. San Diego follows at $277, and Chicago is close behind at $252. At the other end, Austin's median fee is $62 and Dallas's is $75.

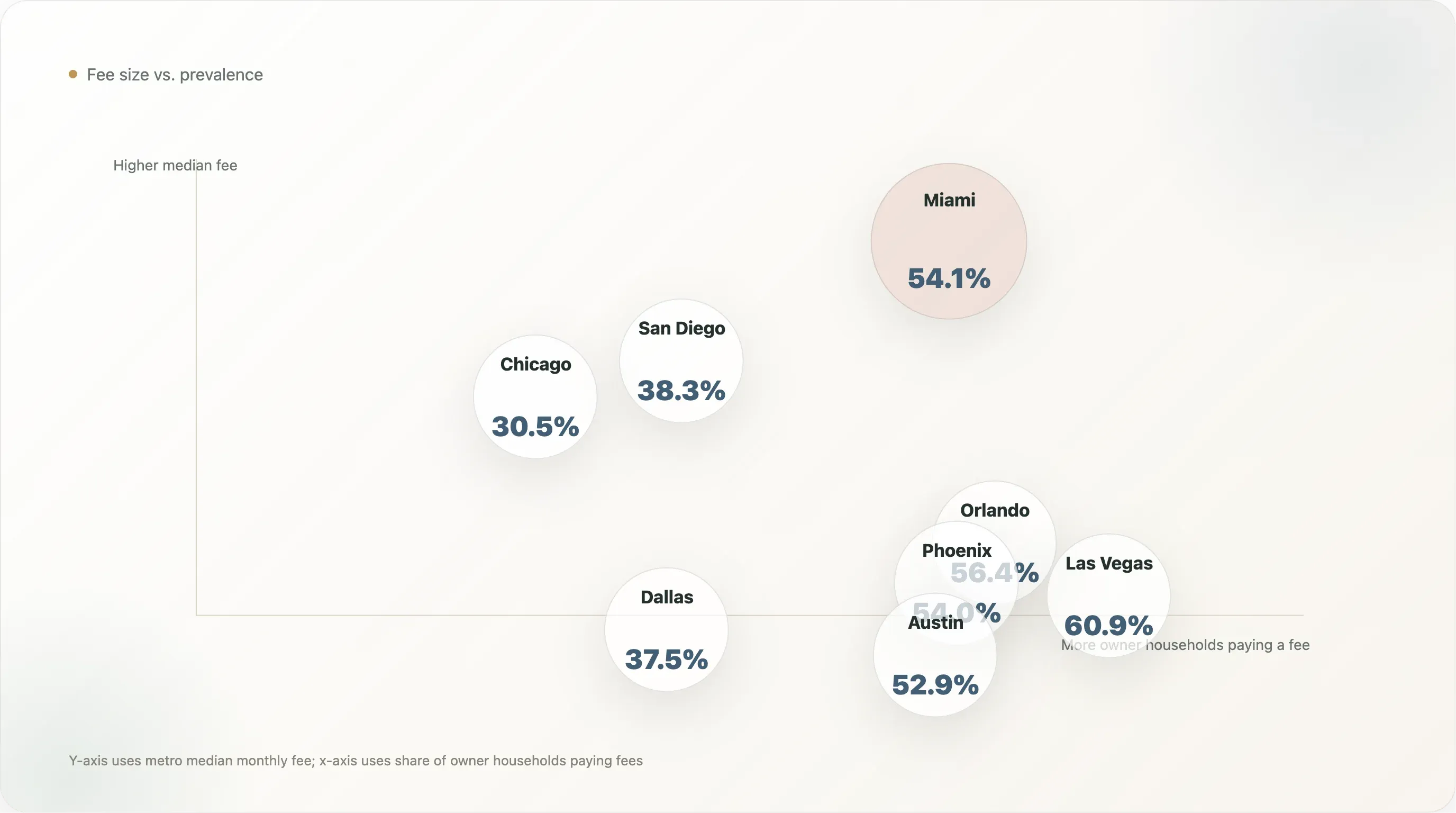

But agents should look beyond the ranking. Las Vegas has a median fee of only $99, but 60.9% of owner-occupied households pay a required fee. Orlando, Phoenix, and Austin also have more than half of owner-occupied households paying a fee. That means agents in these markets should expect HOA to show up frequently in buyer searches, even when typical fees are lower than Miami's.

The First Agent Talking Point: High Fees Change Buyer Psychology

The clearest high-fee market in this group is Miami. The ACS median monthly HOA and/or condo fee is $410. That is $4,920 per year. Over 30 years, without inflation or fee increases, that is $147,600 in nominal payments.

That number can change how a buyer reacts to a property. A buyer may be comfortable with a list price near $500,000, but less comfortable when the true monthly picture includes a $410 fee. This is especially important for buyers who are stretching to qualify, comparing condo and single-family options, or moving from a market where HOA fees are less common.

For agents, the best response is not to frame every high fee as a problem. The better approach is to explain what the fee includes. In a condo building, a higher fee may cover building insurance, exterior maintenance, reserves, elevators, roof, security, water, trash, or shared amenities. In a single-family HOA, the fee may cover landscaping, private roads, gates, common areas, or community amenities.

The question agents can help buyers ask is:

"What costs does this HOA replace, and what risks does it create?"

Miami's high-fee tail makes that question urgent. In the Miami metro, 39.5% of fee-paying owner households report paying $500 or more per month. That represents about 309,627 owner households. This is not a tiny luxury segment. It is a large part of the ownership market.

San Diego and Chicago also have meaningful high-fee tails. In San Diego, 16.8% of fee-paying owner households pay $500 or more per month. In Chicago, the share is 16.2%. Because Chicago is a much larger ownership market, that translates to about 119,755 fee-paying households with $500-plus monthly fees, compared with about 41,508 in San Diego.

Agent takeaway: do not rely on the median alone. If your market has a large high-fee tail, buyers need help understanding both typical fees and outlier fees before they fall in love with a property.

The Second Agent Talking Point: HOA Prevalence Shapes Search Strategy

Some markets are not defined by extreme fee size. They are defined by how often buyers encounter required fees.

Las Vegas is the strongest example in this sample. Its ACS median monthly fee is only $99, but 60.9% of owner-occupied households pay a required HOA and/or condo fee. Orlando is at 56.4%, Phoenix is at 54.0%, and Austin is at 52.9%.

For agents, this changes the search process. In high-prevalence markets, HOA should not be treated as a late-stage disclosure item. It should be built into the buyer's search criteria from the beginning.

That means asking early:

- Is the buyer open to HOA communities?

- What monthly fee range is acceptable?

- Does the buyer value amenities and managed maintenance?

- Does the buyer want fewer restrictions, even if that narrows the search?

- Is the buyer comparing single-family homes, townhomes, and condos on a true monthly basis?

This is especially important in markets with newer planned communities. Realtor.com's 2024 HOA report found that new construction listings were much more likely than existing homes to have HOA obligations. If buyers are focused on newer homes, they may encounter HOA fees more often than expected.

Agent takeaway: in Las Vegas, Orlando, Phoenix, and Austin, HOA is not just a condo issue. It is part of the normal search environment.

The Third Agent Talking Point: Moderate Fees Can Still Be a Big Share of Payment

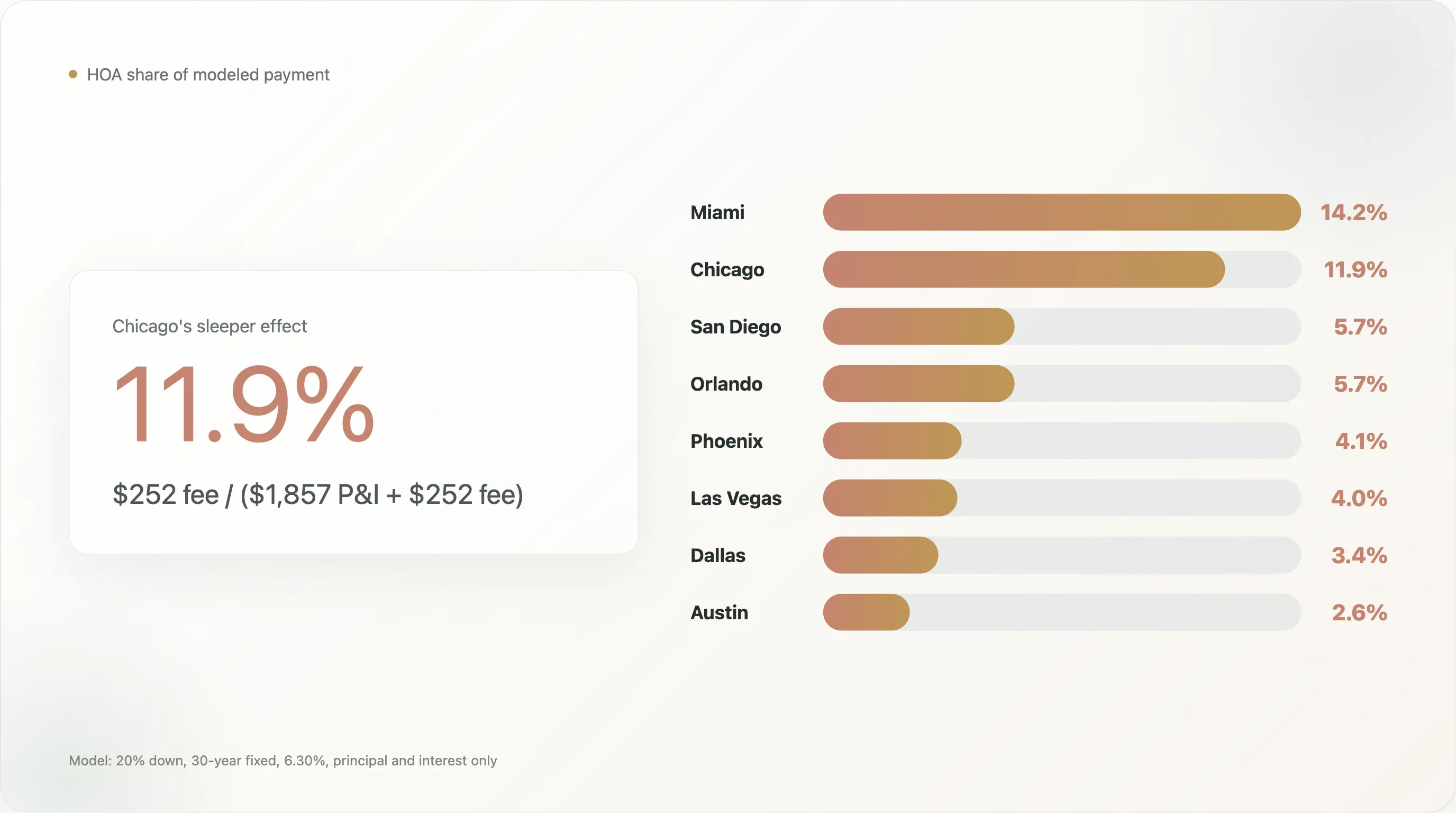

Chicago is the sleeper story in this analysis. It does not have the highest median HOA and/or condo fee. It does not have the highest fee prevalence. But its fee has a large effect on the modeled monthly payment because the metro's April 2026 Realtor.com median listing price is much lower than San Diego's or Miami's.

Using the simple mortgage model, a $375,000 listing price with 20% down creates about $1,857 in monthly principal and interest at 6.30%. Add the ACS median HOA and/or condo fee of $252, and the fee represents 11.9% of the modeled P&I plus HOA payment.

That is a bigger payment share than San Diego, where the median fee is higher in dollar terms but the modeled P&I payment is much larger because the April 2026 median listing price is $933,325. San Diego's $277 median fee represents 5.7% of modeled P&I plus HOA. Chicago's $252 fee represents more than twice that share.

This is the kind of point agents can use to improve buyer counseling. A buyer may see a $252 fee and think it is moderate. But if the property is priced around $375,000, that fee can be a meaningful part of the monthly cost.

Agent takeaway: present HOA as a percentage of the modeled monthly payment, not only as a dollar amount.

Turning HOA Into Buyer-Friendly Language

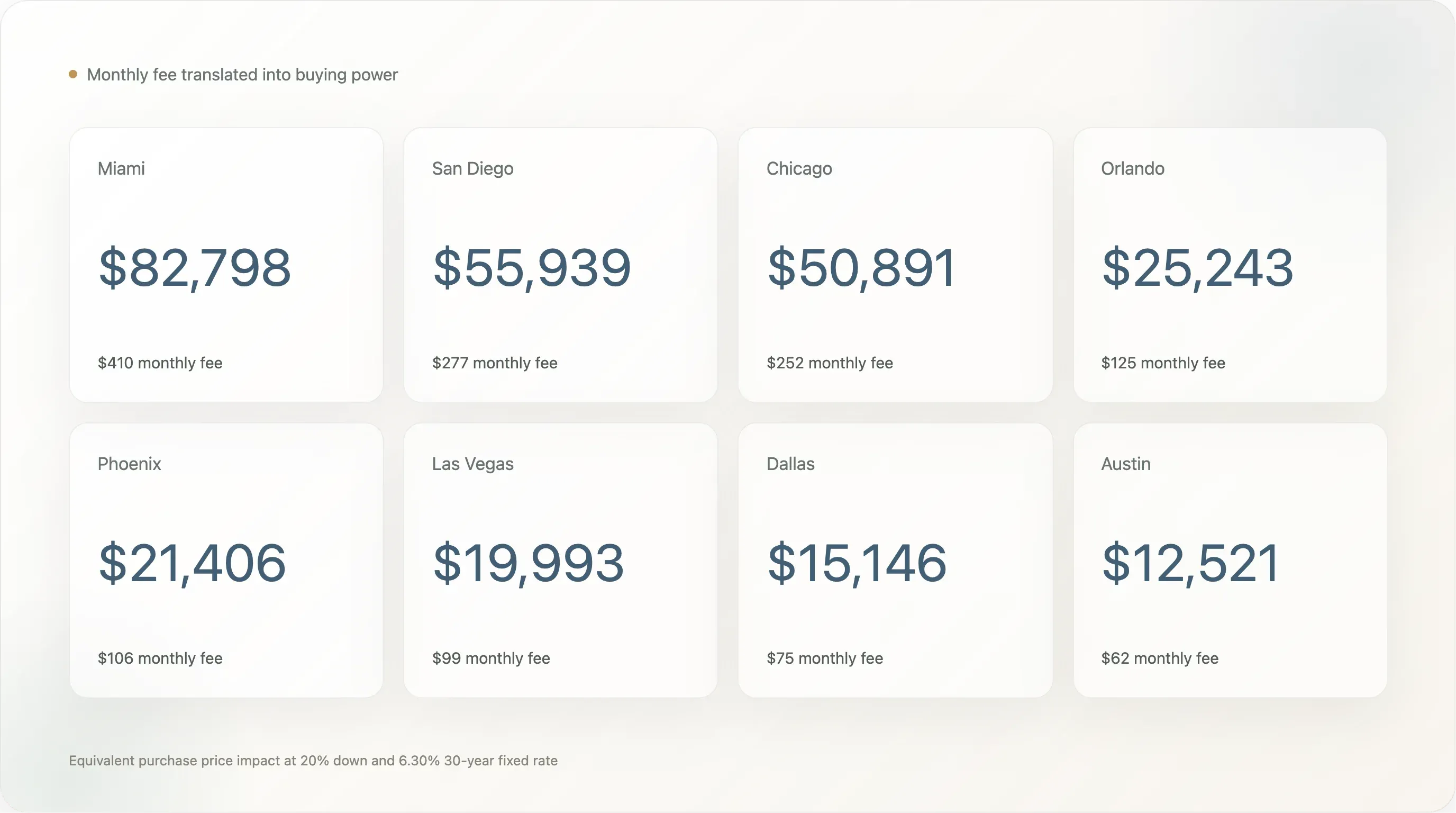

One of the easiest ways to explain HOA is to translate it into buying power.

At a 6.30% 30-year fixed rate, every $100,000 of loan principal costs about $619 per month in principal and interest. Under a 20% down assumption, a monthly HOA fee can be expressed as the purchase price that would create a similar monthly payment.

Using that method:

| Metro | Median monthly HOA/condo fee | Annual fee | 30-year nominal total | Equivalent purchase price at 20% down |

|---|---|---|---|---|

| Miami | $410 | $4,920 | $147,600 | $82,798 |

| San Diego | $277 | $3,324 | $99,720 | $55,939 |

| Chicago | $252 | $3,024 | $90,720 | $50,891 |

| Orlando | $125 | $1,500 | $45,000 | $25,243 |

| Phoenix | $106 | $1,272 | $38,160 | $21,406 |

| Las Vegas | $99 | $1,188 | $35,640 | $19,993 |

| Dallas | $75 | $900 | $27,000 | $15,146 |

| Austin | $62 | $744 | $22,320 | $12,521 |

This framing is not a full financial equivalence. HOA fees can rise, services vary, and HOA payments do not build equity. But it helps buyers understand monthly tradeoffs.

For example:

- In Miami, the $410 median fee has about the same monthly payment impact as adding roughly $82,798 to the purchase price at 20% down.

- In Chicago, the $252 median fee is equivalent to about $50,891 of purchase price.

- In Austin, the $62 median fee is equivalent to about $12,521 of purchase price.

That language can help agents move the conversation away from vague reactions like "this HOA feels high" and toward a concrete comparison: "At this rate and down payment, this fee affects the monthly budget about like buying a home that costs X dollars more."

Agent takeaway: equivalent purchase price is a simple way to make HOA visible in the buyer's monthly budget.

HOA and Market Pressure Are Not the Same Signal

Agents should be careful not to overstate what HOA data proves. Higher HOA fees do not automatically mean more price cuts or longer days on market.

Among the eight metros, Phoenix has the highest April 2026 Realtor.com price-reduced share at 29.1%, but its ACS median HOA and/or condo fee is only $106. Austin has the lowest median fee at $62, yet its price-reduced share is 23.6%. Dallas has a median fee of $75 and a price-reduced share of 22.1%.

Miami has the highest median fee by far at $410 and the longest median days on market at 77 days, but its price-reduced share is 15.7%, lower than Phoenix, Austin, Dallas, Las Vegas, and Orlando.

The practical interpretation is that HOA is one affordability pressure among many. Inventory, seller expectations, insurance, property type mix, job growth, investor activity, new construction, and local price levels all influence DOM and price reductions. HOA can make a buyer's monthly payment harder to absorb, but it does not explain market pressure by itself.

This distinction matters in client conversations. If a buyer asks whether a high HOA means a seller is more likely to negotiate, the honest answer is: maybe, but not automatically. The better question is whether the property's total monthly cost is competitive with nearby alternatives.

Agent takeaway: use HOA to compare total monthly cost, not as a standalone prediction of seller flexibility.

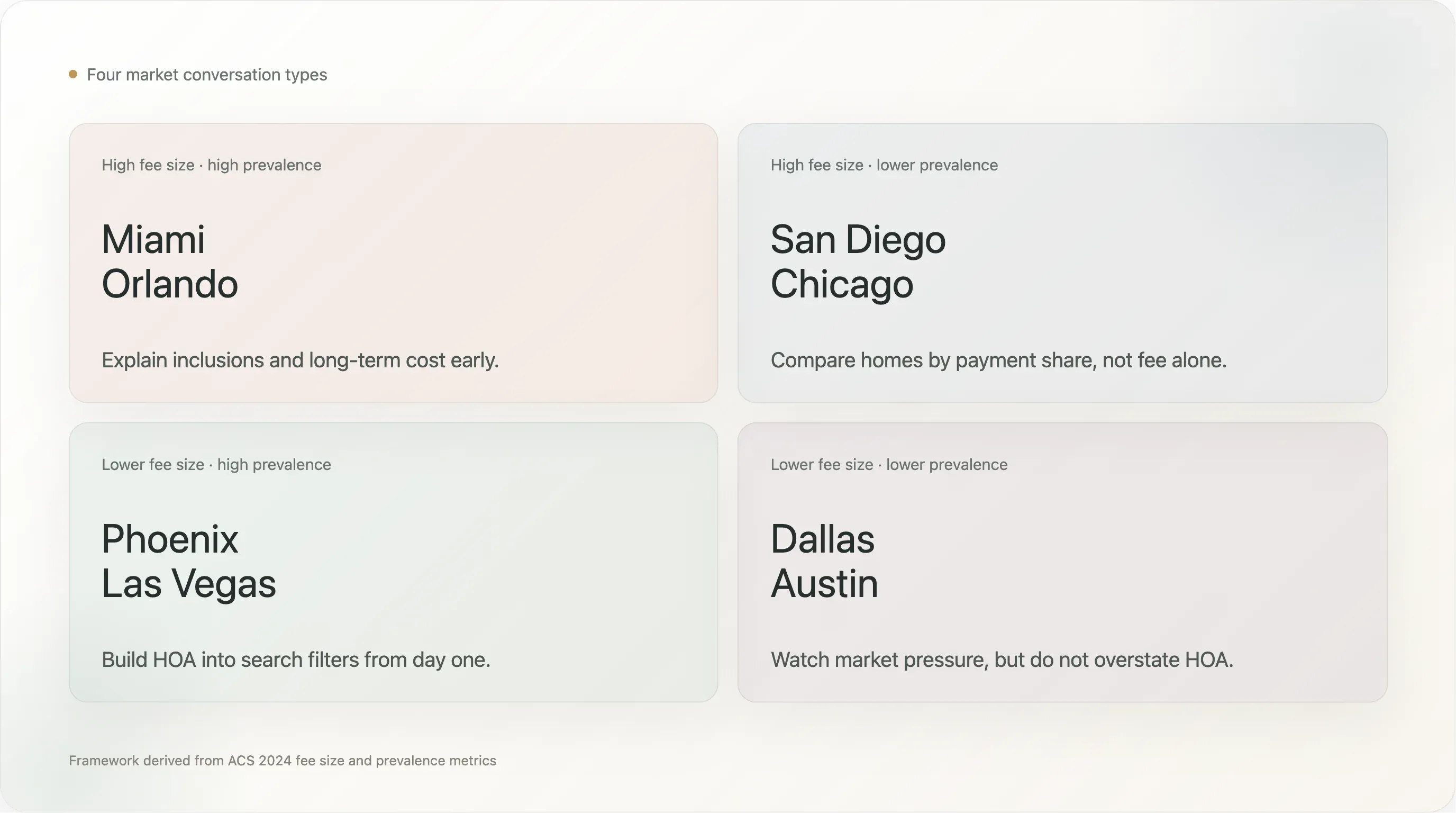

A Four-Quadrant Framework Agents Can Use

The eight metros fall into a useful four-part framework:

| Quadrant | Metros | Agent Interpretation |

|---|---|---|

| High fee size, high prevalence | Miami, Orlando | Buyers are likely to encounter HOA, and the fee can matter meaningfully. Explain inclusions and long-term cost early. |

| High fee size, lower prevalence | San Diego, Chicago | HOA is less universal, but when it appears, it can reshape the monthly payment. Compare by payment share. |

| Lower fee size, high prevalence | Phoenix, Las Vegas | HOA is common, but typical fees are more modest. Build it into search filters from day one. |

| Lower fee size, lower prevalence | Dallas, Austin | HOA is less dominant in the ownership base, though market price-reduction pressure may still be high. |

This framework is more useful than a simple ranking because it maps to different client needs.

A Miami buyer may need help evaluating whether a condo fee is sustainable, whether reserves are adequate, whether building insurance is included, and whether special assessments are possible. A Las Vegas buyer may need to understand that HOA communities are common even if the monthly fee is modest. A Chicago buyer may need to compare a condo and a no-HOA alternative by total monthly payment rather than list price.

Agent takeaway: the right HOA conversation depends on whether the issue is fee size, fee prevalence, or payment share.

Questions Agents Should Ask Before the Buyer Gets Attached

The most useful time to discuss HOA is before a buyer becomes emotionally attached to a property. Once the buyer is already focused on layout, finishes, neighborhood, and commute, a fee surprise can feel like bad news.

Agents can reduce that friction by asking practical questions early:

- What monthly HOA or condo fee range fits your budget?

- Are you comfortable with a higher fee if it includes maintenance, insurance, or utilities?

- Do you prefer lower monthly fees even if that means fewer amenities or more self-managed maintenance?

- Are rental restrictions relevant for your long-term plan?

- Would a special assessment risk change your comfort level?

- Are you comparing condos, townhomes, and single-family homes by total monthly cost?

- Do you want to avoid HOA communities entirely, even if that narrows inventory?

When reviewing a specific property, agents should help buyers verify:

- The current fee and payment frequency.

- What the fee includes.

- Whether there are current or pending special assessments.

- Reserve strength and recent dues increases.

- Litigation, insurance issues, or building-safety concerns.

- Rental restrictions and owner-occupancy rules.

- Whether the condo is warrantable for typical financing.

- Whether the listed fee is confirmed by association documents, not only by a listing field.

This is not legal, financial, or HOA document advice. Buyers should rely on lenders, attorneys, inspectors, association documents, and local professionals where appropriate. But agents can still make the process cleaner by making the right questions visible early.

How Listing Agents Can Position HOA More Clearly

HOA is not only a buyer-agent issue. Listing agents also have a role.

If a property has a high HOA or condo fee, hiding from the number rarely helps. Buyers will find it, lenders will consider it, and the fee will affect the monthly payment conversation. A better listing strategy is to explain what the fee includes in plain language.

For example, instead of only listing "$475 monthly HOA," a listing agent may want the public remarks, flyer, or showing packet to clarify the included services where appropriate:

- Building insurance

- Water, sewer, or trash

- Exterior maintenance

- Roof or structural maintenance

- Landscaping

- Security or concierge

- Pool, gym, clubhouse, or shared amenities

- Reserves or capital maintenance planning

The point is not to oversell the HOA. The point is to help buyers compare apples to apples. If a no-HOA single-family home requires the owner to separately pay for lawn care, exterior maintenance, insurance, roof reserves, and amenities, the monthly comparison is not always obvious.

Listing agents should also be prepared for the opposite issue: if the HOA fee is low, buyers may ask whether reserves are adequate or whether special assessments are likely. Low fees can be a selling point, but only if the association's financial condition supports the story.

Agent takeaway: explain the fee's value, not just the fee's amount.

How Agents Can Replicate This Research Locally

This study was intentionally built with public data and a low token budget. Agents, teams, or brokerages can adapt the approach to their own markets:

- Pull ACS 2024 table B25143 for median monthly HOA and/or condo fee by metro.

- Pull ACS 2024 table B25142 for the count of owner-occupied units with required fees and the fee distribution.

- Pull Realtor.com's public monthly metro inventory CSV for current listing price, active listing count, DOM, and price-reduced share.

- Normalize metro names across the datasets.

- Apply a consistent mortgage assumption, such as 20% down and the latest Freddie Mac PMMS 30-year fixed rate.

- Calculate monthly P&I, P&I plus HOA, HOA share of modeled payment, and equivalent purchase price.

- Turn the result into buyer education content, listing presentation material, or market-update charts.

A brokerage could also build a recurring local dashboard:

- Median HOA and/or condo fee by metro or county.

- Share of owner households paying required fees.

- Share of fee payers above $500 per month.

- Typical fee as a share of modeled monthly payment.

- Equivalent purchase price impact.

- DOM and price-reduction context.

This kind of content is useful because it is not generic market commentary. It helps clients answer a practical question: "What will this home really cost me each month?"

Limitations

This analysis has several limitations.

First, ACS 2024 does not separate HOA fees from condo fees in tables B25142 and B25143. Census explicitly warns that users cannot distinguish whether the monthly fee amount is a homeowners association fee, a condominium fee, or an amount that includes both. For buyer affordability, that combined view is still useful, but the article should refer to "HOA and/or condo fees" when discussing ACS data.

Second, ACS measures owner-occupied households, not active listings. Realtor.com's listing metrics are used only for market context. We should not claim that the median ACS fee is the median fee among homes currently listed for sale in April 2026.

Third, the mortgage model excludes taxes, insurance, mortgage insurance, utilities, maintenance, and closing costs. This is intentional, but it means the modeled payment is not a full cost-of-ownership estimate.

Fourth, the equivalent purchase price calculation is a monthly-payment comparison, not a full financial equivalence. HOA fees do not create home equity, can change over time, and may include services that reduce other costs.

Fifth, metro-level data hides neighborhood and property-type variation. Miami beachfront condos, inland townhomes, Chicago high-rises, Phoenix planned communities, and Dallas single-family subdivisions are very different products. A true listing-level study would need property type, building age, fee inclusions, special assessments, association documents, and financing constraints.

These limitations are important for agents because clients may make property-level decisions from market-level information. Use the data to start better conversations, not to replace property-specific due diligence.

Conclusion

HOA and condo fees are not always a problem. Sometimes they buy useful services. Sometimes they replace costs an owner would otherwise pay directly. Sometimes they support amenities that make a community more desirable.

But they are often underestimated because they sit outside the standard mortgage headline. Buyers may anchor on list price and mortgage rate, then discover late in the search that the HOA line changes the monthly budget.

For agents, this is a chance to provide clearer guidance. In Miami, the median monthly HOA and/or condo fee is large enough to reshape affordability. In Las Vegas, Orlando, Phoenix, and Austin, required fees are common enough that buyers should expect to encounter them frequently. In Chicago, a mid-sized fee can take up a surprisingly large share of the modeled monthly payment because the home price base is lower.

The practical message is simple: help buyers compare homes by true monthly cost. Show the list price, the modeled principal and interest, and the HOA or condo fee together. When the fee is high, explain what it includes. When the fee is low, help buyers ask whether reserves and future assessments could matter. When two homes have different fee structures, translate the fee into equivalent buying power.

The agents who do this well can reduce buyer surprises, improve search quality, and make affordability conversations more concrete. The list price gets attention. The mortgage rate gets headlines. But in many markets, the HOA line is where the monthly payment story changes.

Sources

- 2024 ACS 1-year data API, tables B25142 and B25143, U.S. Census Bureau.

- Nearly a Quarter of Homeowners Paid Condo or HOA Fees in 2024, U.S. Census Bureau.

- Change to Condominium Questions, U.S. Census Bureau.

- Economic Research data library, Realtor.com.

- Monthly metro inventory CSV, Realtor.com.

- Rising HOA Dues Add to Homeowners' Affordability Challenges, Realtor.com.

- Are condo/co-op fees or homeowners' association dues included in my monthly mortgage payment?, CFPB.

- PMMS, Freddie Mac.

- Statistical Review, Foundation for Community Association Research.

Try Thunderbit to Research HOA Costs Faster Get Started Free

Learn More