Let’s be honest: if you’re a financial advisor, you probably didn’t get into this business because you love cold calling or chasing down strangers at networking events. (If you did, I salute you—you’re braver than I am.) But here’s the thing: no matter how sharp your financial planning skills are, your business lives and dies by your ability to generate a steady stream of quality life insurance leads.

I’ve seen firsthand how the right lead strategy can take an advisor from “barely scraping by” to “booked solid for months.” But the world of insurance leads is a jungle—full of overpriced lists, confusing vendor promises, and more acronyms than a government agency. So, whether you’re just starting out or you’ve been around the block a few times, this guide will break down everything you need to know about buying insurance leads, finding free life insurance leads for agents, and using automation tools like Thunderbit to make your lead generation process a whole lot less painful (and, dare I say, even a little fun).

Understanding Life Insurance Leads: Types and Value

Let’s start with the basics: what exactly is a “life insurance lead,” and why does it matter so much for financial advisors?

A life insurance lead is simply a potential client who might be interested in buying a life insurance policy. But not all leads are created equal. In my experience (and, trust me, I’ve seen a lot of spreadsheets), the source and intent behind a lead make all the difference in your conversion rates—and your sanity.

Here’s how I like to break them down:

- Cold Leads: These are folks who haven’t shown any interest in your services. Maybe you bought their info from a generic list or pulled it from a public directory. Conversion rates? Under 2%. You’ll need a thick skin and a strong cup of coffee.

- Warm Leads: These are people who have raised their hand—filled out a quote form, attended your seminar, or were referred by a client. Warm leads can convert at 5–10% or even higher, especially if you follow up quickly.

- Exclusive Leads: These are sold only to you. No other agent is calling this prospect from that source. They cost more—think $75–$150 per lead—but convert about 30% better than shared leads.

- Shared Leads: Sold to multiple agents (sometimes up to 8). They’re cheaper—$10–$40 per lead—but you’ll be racing other advisors to get that first call in.

Pro tip: Warm + exclusive leads are the gold standard. Cold + shared leads? Well, let’s just say you’ll get a lot of practice handling rejection.

Where to Find Life Insurance Leads: Top Channels for Advisors

So, where do you actually get these leads? There’s no shortage of options, but each comes with its own quirks, costs, and conversion rates.

1. Buying from Lead Vendors

The fastest way to fill your pipeline is to buy leads directly from established vendors like EverQuote Pricing, QuoteWizard Pricing, NetQuote Pricing, SmartFinancial Pricing, and Matic Pricing. These platforms run massive marketing campaigns and funnel consumer inquiries straight to your inbox. You can usually choose between exclusive or shared leads, filter by geography or demographics, and sometimes even buy live transfer calls (where the prospect is on the phone, ready to talk).

- Pros: Instant volume, easy to scale, less time spent prospecting.

- Cons: Can get pricey, quality varies, and you’ll need to be fast on the draw (especially with shared leads).

2. Digital Marketing (SEO, SEM, Social Media)

If you’re more of a DIY type, digital marketing is your playground. According to Invoca, 69% of insurance shoppers start online. That means your website, blog, and social media presence matter—a lot.

- SEO: Write helpful articles, optimize for local search, and you’ll attract “free” leads over time (well, free if you don’t count the hours spent tweaking your About page).

- SEM (Google Ads): Be prepared—insurance keywords are some of the most expensive out there, often $50+ per click. But if you know your numbers, you can make it work.

- Social Media: Facebook, LinkedIn, Instagram, even TikTok—wherever your target clients hang out. Personalized messages see higher response rates, and social proof (like reviews) is huge.

3. Offline Events and Direct Mail

Don’t underestimate the classics. Hosting seminars, attending industry events, or sending out direct mailers can yield high-quality leads—especially for certain demographics. In fact, direct mail response rates in insurance are around 3–5%, and 74% of insurance marketers say direct mail delivers the highest ROI compared to other channels (Lob).

- Pros: High trust, less competition in the mailbox.

- Cons: Can be expensive and slow to scale.

4. Cold Calling

Ah, the old-school hustle. It’s not dead, but it’s definitely not for the faint of heart. Conversion rates are low (think 2% or less), but if you’re persistent, you might just catch someone at the right time.

Automating Life Insurance Lead Generation with Thunderbit

Now, let’s talk about making your life easier—because who doesn’t want to spend less time on grunt work and more time closing deals?

I co-founded Thunderbit because I saw how much time advisors waste on repetitive tasks: copying and pasting lead info, organizing spreadsheets, and manually updating lists. Thunderbit is an AI web scraper designed to automate the boring stuff, so you can focus on what actually matters.

How Thunderbit Can Help You:

- 2-Click Scraping: Just open the Thunderbit Chrome Extension, hit “AI Suggest Fields,” and Thunderbit will scan the page, figure out what data to grab, and structure it for you. Then, click “Scrape.” Done.

- AI-Powered Data Structuring: Thunderbit’s AI doesn’t just pull raw text—it organizes names, emails, phone numbers, and more, even if the website’s layout is a mess.

- Scheduled Scraping: Want to keep tabs on a public registry or a vendor’s new leads every week? Set up a scheduled scrape, and Thunderbit will update your data automatically.

- Bypass Export Restrictions: Some platforms make it tough to export your leads. With Thunderbit, you can scrape the data you need, even if there’s no “Download” button.

- Subpage Scraping: Need details from each profile or listing? Thunderbit can visit every subpage and pull extra info—no more clicking through 100 tabs.

Scrape Life Insurance Leads with AI

If you want to see this in action, check out our step-by-step guide or our YouTube channel.

Story time: I once watched an advisor spend an entire afternoon copying leads from a local business directory—by hand. With Thunderbit, that same job takes about five minutes. (And you don’t have to risk carpal tunnel.)

Buying Insurance Leads: How to Choose the Right Vendor

Not all lead vendors are created equal. Some are like the all-you-can-eat buffet—lots of options, but you might regret your choices later. Here’s how to vet vendors before you hand over your credit card:

| Vendor | Lead Types | Price Range (Life) | Exclusivity | Return Policy | Filters/Targeting | Support |

|---|---|---|---|---|---|---|

| EverQuote | Shared/Exclusive/Live Call | $20–$50+ | Shared (up to 3), Exclusive available | 15 days | Yes | Concierge-level |

| QuoteWizard | Shared/Exclusive/Live Call | $20–$30+ | Shared (up to 4), Exclusive available | Very liberal | Yes | Dashboard, agent-friendly |

| NetQuote | Shared/Exclusive | $20–$25 | Both | 10 days | Yes | Real-time delivery |

| SmartFinancial | Shared/Exclusive/Live Transfer | $30–$50+ | Both | 7 days | Advanced | Good customer service |

| Matic | Referral/Embedded | N/A | N/A | N/A | N/A | Partnership model |

Key Criteria:

- Lead Exclusivity: Are you the only one getting this lead, or are you in a footrace with five other agents?

- Pricing: Don’t just look at cost per lead—factor in conversion rates and average policy size.

- Refund Policy: Can you return bad leads (wrong number, fake info, out of territory)?

- Lead Freshness: Are you getting real-time leads, or is this list older than your favorite pair of socks?

- Targeting Options: Can you filter by age, location, coverage type?

- Support: Is there a real person to help if things go sideways?

Pro tip: Start with a small batch from a few vendors, track your results, and double down on what works.

Free Life Insurance Leads for Agents: Are They Worth It?

Who doesn’t love free stuff? (I once drove across town for a free donut. No regrets.) But when it comes to life insurance leads, “free” usually means you’re paying with your time and effort.

Top Sources of Free Leads:

- Referrals: The holy grail. Referral leads convert at 11–30%, and referred clients are 37% more loyal.

- Organic Website Traffic: SEO takes time, but a single blog post can bring in leads for years.

- Social Media Networking: Join local Facebook groups, answer questions on LinkedIn, or even make educational TikToks. (Just don’t ask me to dance.)

- Professional Networking: Build relationships with CPAs, mortgage brokers, attorneys—anyone who can send you warm introductions.

Free vs. Paid Leads

- Quality: Free leads (especially referrals) are often warmer and convert better than cold paid leads.

- Volume: You can’t control the flow. Some months you’ll be swimming in referrals; others, you’ll hear crickets.

- ROI: The cost is low, but you’ll need to invest consistent effort.

Tips to Maximize Free Leads:

- Always ask for referrals after closing a policy.

- Set up a simple referral program (gift cards, charity donations—just keep it compliant).

- Share helpful content online, not just sales pitches.

- Track every lead source so you know what’s working.

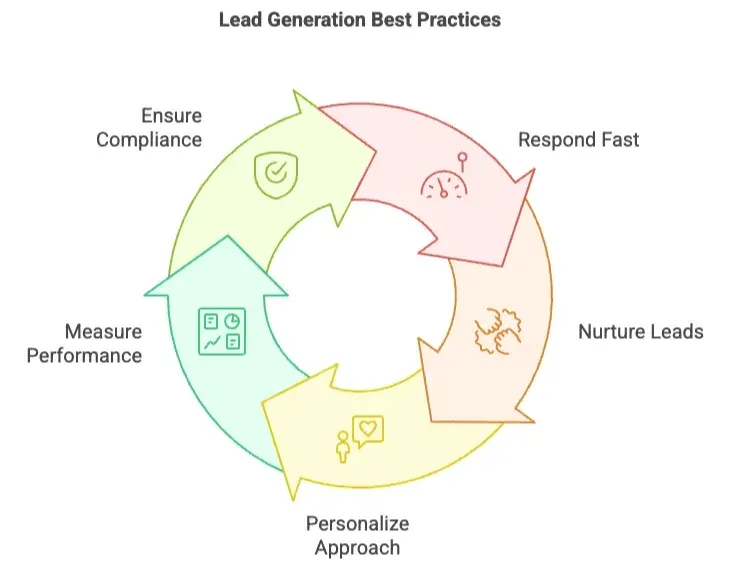

Lead Generation Best Practices for Financial Advisors

Scrape data from any website using AI Get Started Free

AI web scrapers basically mean: ChatGPT reads the whole website and then extracts content based on your need.

Whether you’re buying leads, hustling for referrals, or scraping data with Thunderbit, the fundamentals of good lead generation never change.

- Respond Fast

Speed is everything. Calling a new lead within 1–5 minutes makes you 100 times more likely to connect. Wait an hour, and you might as well be calling from a rotary phone.

- Nurture, Don’t Nag

It often takes 6–8 touches to reach a lead. Use a CRM to track follow-ups, send helpful emails, and mix up your outreach (calls, texts, emails).

- Personalize Your Approach

Nobody wants to feel like “just another number.” Reference the lead’s specific needs, use their preferred communication channel, and always add value before asking for the sale.

- Measure Everything

Track your cost per lead, cost per acquisition, conversion rates, and ROI by source. Use tools like the InsuranceSplash ROI Calculator or a simple spreadsheet.

- Stay Compliant and Ethical

Always honor do-not-call lists, get proper consent for texts/emails, and be transparent about who you are. Compliance isn’t just about avoiding fines—it builds trust.

Exclusive vs. Shared Leads: Making the Right Choice

This is the million-dollar question (sometimes literally). Should you pay more for exclusive leads, or go for volume with shared leads?

Exclusive Leads

- Pros: Higher conversion rates, less competition, smoother sales process.

- Cons: Expensive—$75–$150 per lead, sometimes more.

Shared Leads

- Pros: Cheaper—$10–$40 per lead, more volume.

- Cons: You’re racing other agents, lower conversion rates, more “tire kickers.”

When to choose exclusive: If you’re selling large policies, have a limited budget for time (not money), or want a more predictable close rate.

When to choose shared: If you need to build your pipeline fast, want to practice your sales process, or are working in a less competitive market.

Real talk: Most advisors use a mix—shared leads for volume, exclusive for quality. Track your cost per sale and see what works for you.

Compliance and Ethical Considerations in Buying Insurance Leads

Let’s get serious for a second. The fastest way to tank your reputation (and rack up some hefty fines) is to ignore compliance.

- TCPA: Don’t call numbers on the Do Not Call Registry. Get written consent for texts and auto-dialers. The FCC’s new rules require explicit, one-to-one consent.

- CAN-SPAM: Every marketing email must have an unsubscribe link and your physical address. No misleading subject lines.

- Data Privacy: If you’re in California (or dealing with CA residents), know the CCPA. Always honor data deletion requests.

- Ethics: Be honest about who you are, respect opt-outs, and don’t use high-pressure tactics.

Tip: Always ask your lead vendors how they collect consent. If they can’t answer, run.

Measuring Success: Tracking ROI from Life Insurance Leads

If you’re not tracking your numbers, you’re flying blind. Here’s how to keep your lead gen profitable:

- Log Every Lead Source: Use a CRM or spreadsheet to track where each lead came from and what happened.

- Calculate Cost Per Lead and Cost Per Sale: Don’t just look at how many leads you bought—track how many turn into clients.

- Measure Conversion Rates: Lead-to-appointment, appointment-to-sale, and overall lead-to-sale.

- ROI Formula: ROI = (Total Revenue from Sales – Total Cost of Leads) / Total Cost of Leads

- Adjust and Optimize: Shift budget to the sources with the best ROI. Drop what’s not working.

Example: If you spend $1,000 on leads and earn $3,000 in commissions, your ROI is 200%. If you’re only breaking even, it’s time to tweak your strategy.

Key Takeaways and Next Steps for Financial Advisors

Let’s wrap it up with the essentials:

- Know your lead types: Cold, warm, exclusive, shared—each has its place.

- Choose the right channels: Mix paid, free, digital, and traditional methods.

- Leverage automation: Tools like Thunderbit can save you hours and help you scale smarter, not harder.

- Track your ROI: Measure everything, optimize relentlessly.

- Stay compliant: Respect privacy, consent, and ethical standards.

The best advisors aren’t the ones who buy the most leads—they’re the ones who experiment, track results, and keep learning. So try out different approaches, automate what you can, and don’t be afraid to ask for help (or for referrals).

And if you’re tired of copy-pasting leads until your fingers go numb, give Thunderbit a spin. Your future self—and your wrist—will thank you.

Automate Lead Collection with Thunderbit

Want more tips on web scraping, lead generation, and automation? Check out the Thunderbit Blog, including guides like How to Scrape Website Data into Excel using AI and The Best Web Scraping Tools & Software in 2025.

Happy hunting—and may your leads be warm, exclusive, and ready to buy. (Or at least not hang up on you immediately.)

Try AI Web Scraper Get Started Free

FAQs

-

What are life insurance leads and why should advisors buy them?

A life insurance lead is a prospect who’s shown interest in purchasing a policy—whether by filling out a quote request, attending a seminar, or being referred. Buying leads gives you immediate access to interested prospects rather than starting from cold lists, helping you:

- Boost conversion rates: Warm or exclusive leads often convert at 5–30%, versus under 2% for cold outreach.

- Save time: Skip hours of research and data entry by purchasing curated lists.

- Target precisely: Vendors let you filter by age, location, income, or coverage need, so you focus on the most qualified prospects.

-

How does Thunderbit’s “AI Suggest Fields” streamline scraping life insurance lead data?

Thunderbit’s “AI Suggest Fields” feature lets you open any lead-vendor webpage, click a button, and type the fields you need (e.g., name, phone, email, coverage interest). The AI automatically analyzes the page’s structure, sets up those columns, and eliminates manual HTML or selector work. Instead of spending hours mapping data points, you get a structured table ready for export in seconds—so you can load leads into your CRM and start calling immediately.

-

How can Thunderbit’s scheduling and subpage scraping optimize lead management?

With Thunderbit, you can schedule recurring scrapes (daily or weekly) on your favorite lead sources to keep data fresh without lifting a finger. Its subpage scraping follows every profile or quote detail link, extracting deeper information—like policy type, budget range, or referral notes—and merges it into one table. This ensures you always have up-to-date, comprehensive lead profiles in your CRM, reducing manual upkeep and helping you prioritize follow-ups based on the latest data.

Learn More: