Let me take you back to a moment not so long ago: I’m sitting in a coffee shop, laptop open, and I overhear a conversation at the next table. Two folks are deep in discussion about “buying mortgage leads”—one is a loan officer, the other a real estate agent. They’re tossing around numbers, talking about “exclusive leads,” “refi leads,” and the best way to follow up. It hit me: mortgage leads aren’t just a buzzword—they’re the lifeblood of the mortgage and real estate industry. Whether you’re a broker, lender, or agent, understanding mortgage leads is the difference between chasing your tail and actually closing deals.

What Is Data Scraping and How to Do It in 2025 Get Started Free

The mortgage market is always shifting. After the wild ride of the pandemic boom, the U.S. mortgage industry cooled off, but it’s rebounding. In 2024, new mortgage originations are expected to hit nearly $1.8 trillion, with forecasts pointing to a 28% jump in 2025. That’s a lot of people looking for loans—and a lot of competition to win their business. So, what exactly are mortgage leads, why are they so valuable, and how do you get the good ones? Let’s break it down, jargon-free.

What Are Mortgage Leads? A Simple Breakdown

At its core, a mortgage lead is just a person—someone who’s shown interest in a mortgage product. Maybe they want to buy their first home, refinance their current loan, tap into their home equity, or explore a reverse mortgage. What makes them a “lead” is that they’ve raised their hand in some way: filled out an online form, clicked on an ad, responded to a referral, or even just engaged with a lender’s social media post.

Think of mortgage leads as the digital equivalent of someone walking into a bank and asking, “Can you tell me about your home loans?” That moment of interest is gold for lenders and brokers, because it’s the first step toward a potential deal.

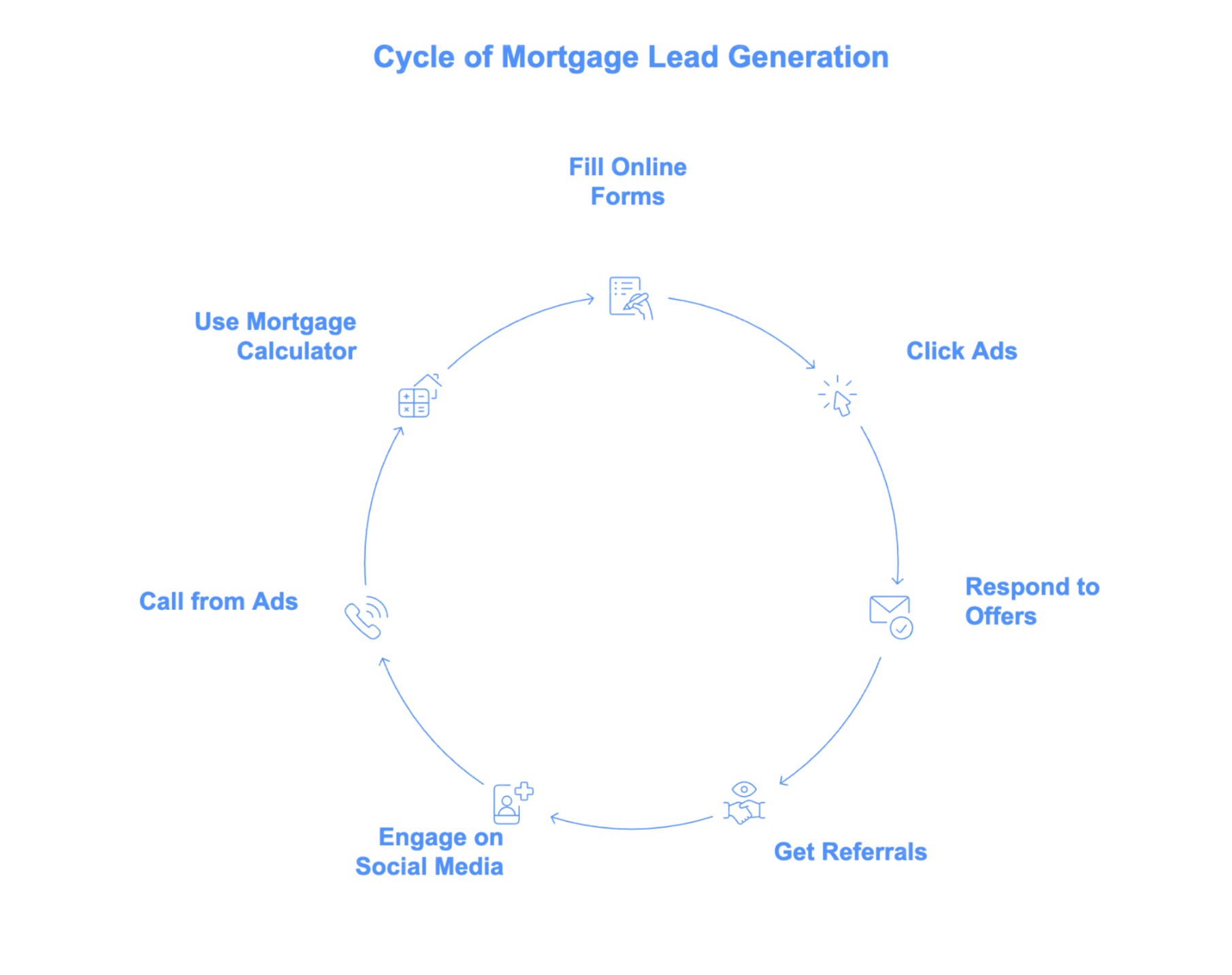

How Do People Become Mortgage Leads?

- Filling out online applications or pre-qualification forms

- Clicking on ads (Google, Facebook, Instagram—you name it)

- Responding to email or direct mail offers

- Getting referred by a friend, agent, or past client

- Engaging with mortgage content on social media

- Calling a number from a TV or radio ad

- Using a mortgage calculator and submitting their info for results

Any time someone provides their contact information and signals they’re interested in a mortgage, that’s a lead. For lenders, every lead is a potential business opportunity—some hotter than others, but all worth a look.

Types of Mortgage Leads: Not All Leads Are the Same

Not all mortgage leads are created equal. Just like you wouldn’t wear flip-flops to a snowstorm (unless you’re braver than me), you shouldn’t treat every lead the same way. The type of mortgage lead depends on what the customer needs and where they are in their journey.

Purchase Mortgage Leads

These are the folks looking to buy a home—first-timers, move-up buyers, or even seasoned investors. In today’s market, purchase loans make up the lion’s share of activity (about 76% of mortgages in 2024). The typical purchase lead might be a millennial couple browsing listings online or a retiree downsizing to a condo. They’re often doing a ton of research, comparing rates, and looking for guidance—so speed and education are key.

Refinance Mortgage Leads

Refi leads are current homeowners looking to swap out their old mortgage for a new one—maybe to get a lower rate, maybe to pull out some cash. After the refinance boom of 2020–2021, refi activity slowed way down as rates rose, but it’s ticking up again as some folks look to consolidate debt or fund big expenses (cash-out refis are especially popular). These leads are often older, equity-rich, and very sensitive to interest rates.

Home Equity Leads

Homeowners who want to tap into their home’s value without refinancing the whole mortgage go for home equity loans or HELOCs. In 2023–24, about 57% of new HELOC borrowers were over age 50. These leads are often motivated by home renovations, medical expenses, or big-ticket purchases. With so many homeowners “locked in” at low rates, HELOCs are a hot topic.

Reverse Mortgage Leads

Reverse mortgage leads are a unique group: homeowners aged 62 and up who want to turn their home equity into cash—without monthly payments. The average reverse mortgage borrower is about 74–75 years old. These leads require a lot of education and trust-building, and often involve family members in the decision.

Where Do Mortgage Leads Come From? Key Sources Explained

Mortgage leads don’t just fall from the sky (though wouldn’t that be nice?). They’re generated through a mix of digital marketing, content, referrals, and sometimes good old-fashioned hustle.

Here’s where most leads originate:

Online Advertising for Mortgage Leads

Platforms like Google Ads and Facebook are the bread and butter for many lenders. Search ads target people actively looking for “mortgage rates” or “home loan quotes”—these are high-intent leads, but competition is fierce. The average cost-per-click for “mortgage” on Google is about $47, and a single lead can cost $50–$100 or more. Social media ads (Facebook, Instagram) let you target by age, location, or life events, and typically run $10–$40 per lead, though quality can be hit or miss.

SEO and Content Marketing

Ever Googled “best mortgage lender in Dallas” or “how much house can I afford?” That’s SEO at work. Lenders and finance sites like NerdWallet and Bankrate publish helpful articles, calculators, and guides to attract organic traffic. These leads are “free” in the sense that you’re not paying per click, but building up that content takes time and effort. The upside? SEO leads are often high-intent and trust your brand.

Social Media and Referrals

Loan officers and agents who are active on LinkedIn, Facebook, or even TikTok can generate a steady trickle of inbound leads by sharing tips, stories, and testimonials. Referrals—from past clients, friends, or real estate partners—are the gold standard. They convert at much higher rates (sometimes 20% or more), but they take time to build up and aren’t as easy to scale.

Buying Mortgage Leads

If you want to fill your pipeline fast, you can buy leads from third-party vendors. The “big four” are Bankrate, LendingTree, NerdWallet, and SmartAsset. Bankrate leads are pricey ($200–$250 each) but high quality; LendingTree sells shared leads for $20–$50, but you’ll be competing with other lenders for the same prospect. There are also niche vendors for VA, FHA, or reverse mortgage leads. Just remember: not all vendors are created equal, and you need a solid follow-up system to make the most of purchased leads.

Who Needs Mortgage Leads? The Key Players

Mortgage leads aren’t just for banks. Here’s who’s in the game:

Mortgage Brokers and Lenders

Brokers and lenders are the primary buyers and users of mortgage leads. Their business depends on converting leads into closed loans. Whether they’re running their own ads or buying from vendors, leads keep their pipeline full—especially during slow periods or when launching into new markets.

Real Estate Agents and Fintech Companies

Agents often partner with lenders to share leads—helping buyers get pre-approved and making sure deals close smoothly. Some agents even buy mortgage leads themselves, hoping to win the buyer’s real estate business in return. Fintech companies (think online mortgage marketplaces or digital lenders) treat leads as a data science problem, generating and nurturing leads at scale through apps and websites.

Marketing Agencies

Many small lenders and brokers outsource their lead generation to marketing agencies. These agencies run ads, manage SEO, and sometimes even negotiate with lead vendors. Their job is to deliver qualified leads and set up systems (like CRMs and automation) to help clients manage and convert those leads efficiently.

How to Evaluate Mortgage Leads for Quality

Here’s the cold, hard truth: not all leads are worth your time. Some are just “tire kickers,” others are ready to close tomorrow. So how do you tell the difference?

What Makes a Quality Mortgage Lead?

- Verified contact info: Phone and email actually work, and the person responds.

- Clear intent and timeline: They want to buy or refinance soon—not “maybe next year.”

- Basic eligibility: Decent credit, steady income, some down payment or equity.

- Loan need matches your offerings: If you only do FHA loans, a jumbo loan lead isn’t a fit.

- Geographic match: You need to be licensed where the lead is located.

Most raw leads won’t meet all these criteria, which is why mortgage lead close rates are often around 3%. The trick is to qualify leads quickly—filtering out the “looky-loos” and focusing on the ones who are ready and able to move forward.

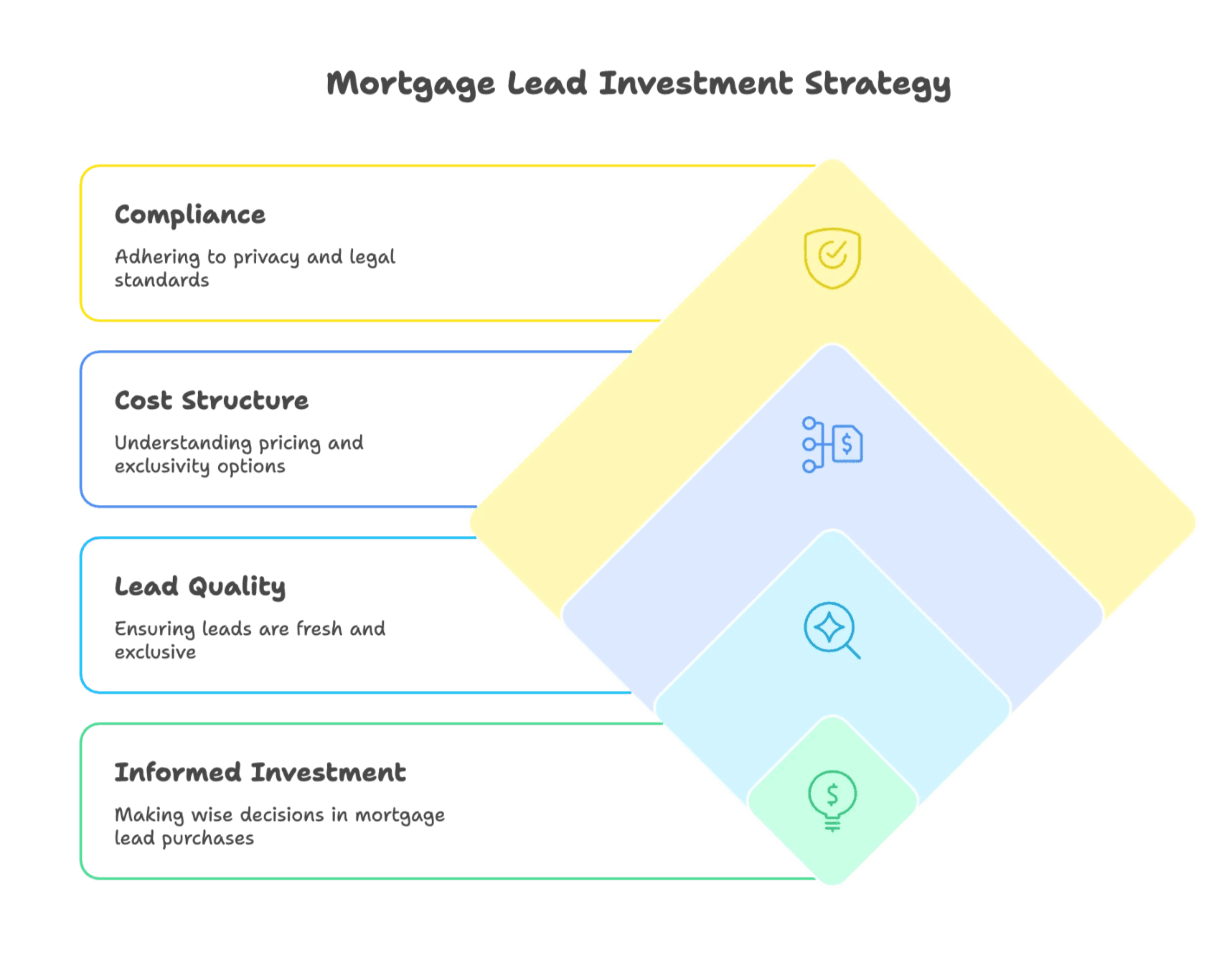

Mortgage Leads for Sale: What to Know Before You Buy

Buying mortgage leads can be a shortcut to a full pipeline, but it’s not without risks. Here’s what you need to know:

How Does Buying Mortgage Leads Work?

You pay a vendor (like Bankrate or LendingTree) for access to leads—either exclusive (sold only to you) or shared (sold to multiple lenders). Prices vary widely: standard purchase loan leads might run $20–$100, VA or reverse mortgage leads $50–$150, and jumbo loan leads $100–$200 or more (see typical costs here). You’ll usually get contact info, loan need, and sometimes basic qualifying details.

Reputable sources for mortgage leads include:

- Bankrate

- LendingTree

- NerdWallet

- SmartAsset

- Niche providers like FreeRateUpdate, Mortgage Research Center (for VA leads), and LeadPoint

Key considerations before buying:

- Lead exclusivity: Exclusive leads cost more but face less competition.

- Lead freshness: The sooner you get the lead after they submit info, the better.

- Refund policy: Can you return bogus or unqualified leads?

- Compliance: Make sure you’re following do-not-call and privacy laws.

Best Practices for Managing and Converting Mortgage Leads

So you’ve got a stack of leads—now what? Here’s how to turn those names and numbers into closed loans (and maybe a few happy dances):

-

Respond Fast—Like, Really Fast

Speed is everything. Responding within 5 minutes makes you 21 times more likely to convert a lead. Wait an hour, and you’re yesterday’s news. If you can’t call right away, set up an automated text or email to let them know you’ll be in touch soon. -

Use Multiple Channels

Not everyone picks up the phone. Try a mix of calls, texts, and emails. Some folks prefer texting, especially younger buyers. Others want a phone call or a detailed email. Meet them where they are. -

Personalize Your Outreach

Reference their specific needs: “I see you’re looking to refinance your $300K loan—let’s talk about your options.” Personalization shows you’re paying attention and builds trust. -

Be Persistent (But Not Annoying)

It often takes 5 or more follow-ups to close a deal. Have a system: call, text, email, repeat. But always add value—share tips, answer questions, and don’t just spam “Are you ready yet?” messages. -

Use a CRM and Automate Where You Can

A good CRM is your best friend. It tracks every lead, logs every call, and reminds you to follow up. Automation can handle the routine stuff (like drip emails), so you can focus on the personal touch.

-

Educate and Advise

Don’t just sell—help. Share guides, calculators, or market updates. Position yourself as a resource, not just a salesperson. -

Measure and Refine

Track your contact rates, conversion rates, and which channels work best. Adjust your approach based on what actually gets results.

Mortgage Leads for Sale: What to Know Before You Buy

Let’s talk turkey: buying mortgage leads is a big investment. Here’s what you need to know before you open your wallet:

- What’s included: Usually name, contact info, loan need, sometimes credit or property details.

- Pricing: Standard leads run $20–$100, VA or reverse mortgage leads $50–$150, jumbo leads $100–$200+ (see more pricing info).

- Exclusive vs. shared: Exclusive leads cost more but you’re the only one calling. Shared leads are cheaper but you’ll need to be quick on the draw.

- Lead freshness: The faster you get the lead after they submit info, the better your odds.

- Refunds: Make sure you can return bad leads.

- Compliance: Stay on the right side of privacy and do-not-call laws.

The Future of Mortgage Leads: Trends to Watch

Mortgage lead generation is changing fast. Here’s what’s on the horizon:

AI-Driven Targeting and Automation

Artificial intelligence is making it possible to spot likely borrowers before they even start shopping. Predictive analytics, AI chatbots, and automated lead scoring are already helping lenders engage leads faster and more effectively (see industry trends).

Changing Consumer Behavior

Younger buyers (hello, Gen Z) expect instant responses, prefer texting, and want to do as much as possible online. If you’re still relying on cold calls and paper forms, you’re going to get left behind.

Omnichannel and Personalized Marketing

Consumers want a seamless experience—start a chat on your website, get a follow-up text, and pick up the conversation by phone. Integrating your channels and personalizing your outreach is the new standard.

Regulatory and Market Shifts

Privacy concerns and potential bans on “trigger leads” (where credit bureaus sell your info when you apply for a mortgage) could shake up the market. Lenders will need to double down on consent-based, relationship-driven marketing.

Conclusion: Key Takeaways on Mortgage Leads

Scrape Real Estate and Mortgage Leads with AI Get Started Free

Mortgage leads are the fuel that keeps the mortgage industry running. Whether you’re a broker, lender, agent, or fintech startup, understanding the types of leads, where they come from, and how to work them is essential. Not all leads are created equal—focus on quality, respond fast, personalize your approach, and use technology to stay organized.

The future? It’s all about speed, personalization, and smart use of data. AI and automation are making it easier to find and engage the right prospects, but the human touch—being helpful, responsive, and trustworthy—still wins the day.

So next time you hear someone talking about mortgage leads at the coffee shop, you’ll know exactly what’s at stake—and maybe you’ll even have a few tips to share.

Try Thunderbit for Real Estate Lead Scraping

FAQs

What is a mortgage lead?

A mortgage lead is a person who has shown interest in a home loan by submitting contact info—online forms, ads, referrals, etc.—signaling they may need mortgage services soon.

Are all mortgage leads the same?

No. Leads vary by type: purchase, refinance, home equity, and reverse mortgage. Each has different customer profiles, timelines, and needs.

Is it better to buy exclusive or shared leads?

Exclusive leads cost more but reduce competition. Shared leads are cheaper but often go to multiple lenders, so fast follow-up is crucial.

How do I increase lead conversion?

Respond within 5 minutes, personalize outreach, use multiple channels (text, call, email), and automate follow-ups using a CRM.

Read More

-

Mortgage Lead Cost: How Much Are Mortgage Leads in 2025? – Phonexa

- Breakdown of lead pricing by type (FHA, VA, jumbo, reverse), plus tips on maximizing ROI when buying leads.

-

Mortgage Lead Generation: How to Win and Keep Clients – Morty

- Strategies for winning clients through referrals, content, and digital engagement—great for brokers and agents.

-

Mortgage Statistics – LendingTree

- Up-to-date stats on originations, refinance activity, and borrower demographics shaping today’s mortgage landscape.

-

Speed to Lead: What A Minute Means to Your Online Mortgage Leads

- Data-backed guide on why fast, multi-channel response dramatically improves lead conversion for mortgage professionals.

Try AI Web Scraper for Real Estate and Mortgage Leads Get Started Free